By Rodney Hobson from interactive investor.

The proof of the pudding lies with a new chief who looks set to sell off poor performers to boost spending on premium lines.

A heavy burden lies on the shoulders of Miguel Patricio, who took over as chief executive officer of food and beverage giant Kraft Heinz (NASDAQ:KHC)last month. The reputation of famed investor Warren Buffett depends on him – as well as the immediate future of Kraft itself.

Patricio has form, having rescued the struggling Chinese business of brewer Anheuser-Busch InBev (NYSE:BUD), but he has his work cut out taking on Krafts whole global range including condiments and sauces, cheese and dairy, meals, meat, refreshment beverages and other grocery products.

Its hard to believe that Kraft in its pomp made a brief if somewhat half-hearted attempt to take over Anglo-Dutch rival Unilever (LSE:ULVR) in 2017. Now it faces selling off some of its brands to finance the development of the ones with better prospects.

Since rival food groups H J Heinz and Kraft Food Group merged in 2015 to form the enlarged group with headquarters in Chicago and Pittsburgh, sales have struggled and margins have been squeezed. It has been affected to some extent by a trend towards foods perceived as healthier than tomato ketchup and baked beans; on the other hand there has been increased competition from cheaper alternatives.

Critics claim that the response of management was to cut costs rather than invest in existing products and widen the range, backed with corresponding advertising campaigns. As sales failed to improve, prices were slashed to boost revenue, but reduced margins meant there was no improvement to the bottom line.

Meanwhile, the combined headcount was reduced by more than a quarter, which cut duplicated costs but also caused uncertainty among key staff and is perhaps the reason why the company failed to make as much headway as shareholders hoped.

So far this year Kraft Heinz has become the subject of a US Securities and Exchange Commission investigation, has reduced in its dividend by a third to $1.60 and has written down the value of its Kraft and Oscar Meyer brands by $15.4 billion.

Patricios main tactic at InBevs Chinese arm was to promote Budweiser, the flagship brand, and he could well repeat this tactic at Kraft Heinz by throwing extra marketing behind key products while improving their margins.

Source: TradingView Past performance is not a guide to future performance

Since Krafts heavy debt pile, $30.8 billion at the end of last year, offset by only $1.1 billion cash, will act as a restraint, he is likely to sell off the poorer performers, hopefully without giving the impression of conducting a fire sale. Already the Canadian cheese business has been sold and other lines are being touted round. These sales could even help to finance selective acquisitions.

Watching developments will be Warren Buffet, chief executive officer of investment fund Berkshire Hathaway (NYSE:BRK.A), which now owns 26.7% of Kraft Heinz, its biggest equity investment. Berkshire and Brazilian private equity group 3G Capital acquired Kraft Foods Group in 2013 for $10 billion and Buffett has since said he paid too much, although he continued to feel that Kraft was “a wonderful business”. Berkshire also bought Heinz for $23 billion, a price that with hindsight Buffett thought was fair.

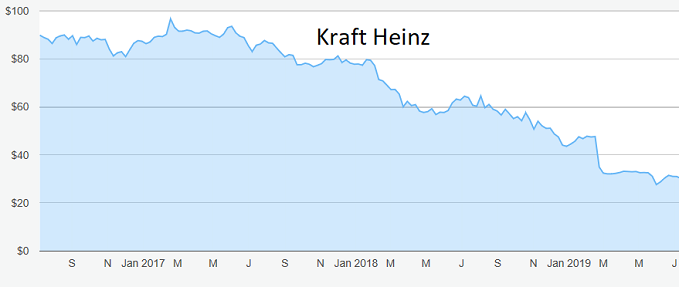

Kraft Heinz shares peaked at $96.65 in February 2017 and have been sliding ever since to stand at just above $30 now. They hit a low of $26.96 in May but $30 seems to be a floor unless there is further bad news.

Analysts are cautious. Most rate the stock a hold but the consensus is that a rise of about $4 is all that shareholders can hope for over the next 12 months.

However, the price-earnings ratio is undemanding at 10 while, despite the dividend cut, the yield is a very attractive 5.3%.

Hobsons choice: Buy at up to $32, bearing in mind that this is a moderately risky investment.

Rodney Hobson is a freelance contributor and not a direct employee of interactive investor.

Rodney Hobson is an experienced financial writer and commentator who has held senior editorial positions on publications and websites in the UK and Asia, including Business News Editor on The Times and Editor of Shares magazine. He speaks at investment shows, including the London Investor Show, and on cruise ships. His investment books include Shares Made Simple, the best-selling beginners guide to the stock market. He is qualified as a representative under the Financial Services Act.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrumRead More – Source

{kind=link}